For years, Class III milk was the price leader when it comes to milk prices, but that has flipped, says Corey Geiger, lead dairy economist for CoBank.

“The Class IV milk price was the price leader in 2023 and likely will be the leader in 2024,” Geiger says.

The Class III milk price for December was $16.04 per cwt, while the Class IV milk price was $19.23. Class III milk is made into cheese, while Class IV milk includes butter and full-fat dairy products, which have been surging in popularity.

“In 2023, about 60% of the value in milk checks came from butterfat,” Geiger says. “It usually comes from protein. The last time we saw that was in 2017. I think that will continue in 2024 because everyone loves butter and full-fat dairy products.”

Class III milk prices are down, and that impacts prices for Midwest milk, which is mostly made into cheese. Geiger says the U.S. has a number of new cheese plants. As these plants come on line, he expects cheese prices to recover in the second half of the year.

Geiger believes we need to clear the global market of cheese.

“The U.S. currently has the lowest cheese prices in recent years,” he says. “The price looks better the second half of 2024. All the futures prices for Class III milk from June through December are over $18 per cwt. For Class IV milk prices, everything this year is over $19, and there are some months next fall above $20 per cwt.”

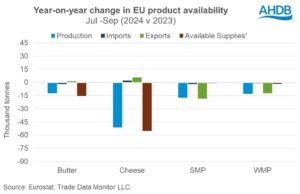

Geiger says U.S. cheese exports were down 4.5% from January through October 2023 compared to the same time in 2022. In Europe, cheese exports are up 2.4%, and in New Zealand, they are up 19%.

“Right now, U.S. cheese prices are the lowest of the Big 3 [U.S., Europe and New Zealand], and that will likely increase U.S. cheese sales. Right now, the strong U.S. dollar isn’t helping U.S. exports,” Geiger explains.

Shipping costs rising

Geiger is concerned about the conflict in the Middle East heating up and causing shipping costs there to rise.

“Logistics company Maersk announced on Jan. 2 that it would be pausing all transit through the Red Sea and the Gulf of Aden until further notice,” Geiger says. “This decision follows an attack on the company’s vessel on Dec. 30. This will significantly raise shipping costs as some shipping fleets avoid the Suez Canal and go around the tip of Africa. This longer journey can cost another 10 days on the seas.”

Too few dairy heifers

USDA is projecting 0.9% growth in U.S. milk production in 2024. Geiger believes milk growth is being held back in the U.S. by a shortage of replacement heifers.

“There are not many dairy replacements out there with all of the growth in beef on dairy,” Geiger says. “A year ago, replacement heifers were selling for $1,400 to $1,500 each, and now they are as high as $2,500 to $2,800.”

Globally, milk production continues to be tepid. In the European Union and United Kingdom, October milk was down 1.7% year over year. Milk production in Ireland, a major exporting country, dropped 12.6% in October. In the U.S., November milk slid 0.6%, largely due to 44,000 fewer dairy cows than one year earlier.

Once December numbers are tallied, U.S. milk may only move a paltry 0.2% over 2022 levels, Geiger says.